At What Age Do You Have To Draw From Your 401k

Are you looking for a 401(chiliad) savings guide? This mail will go through how much I think you should have in your 401(k) past age in order to have a comfy retirement in your 60s and beyond.

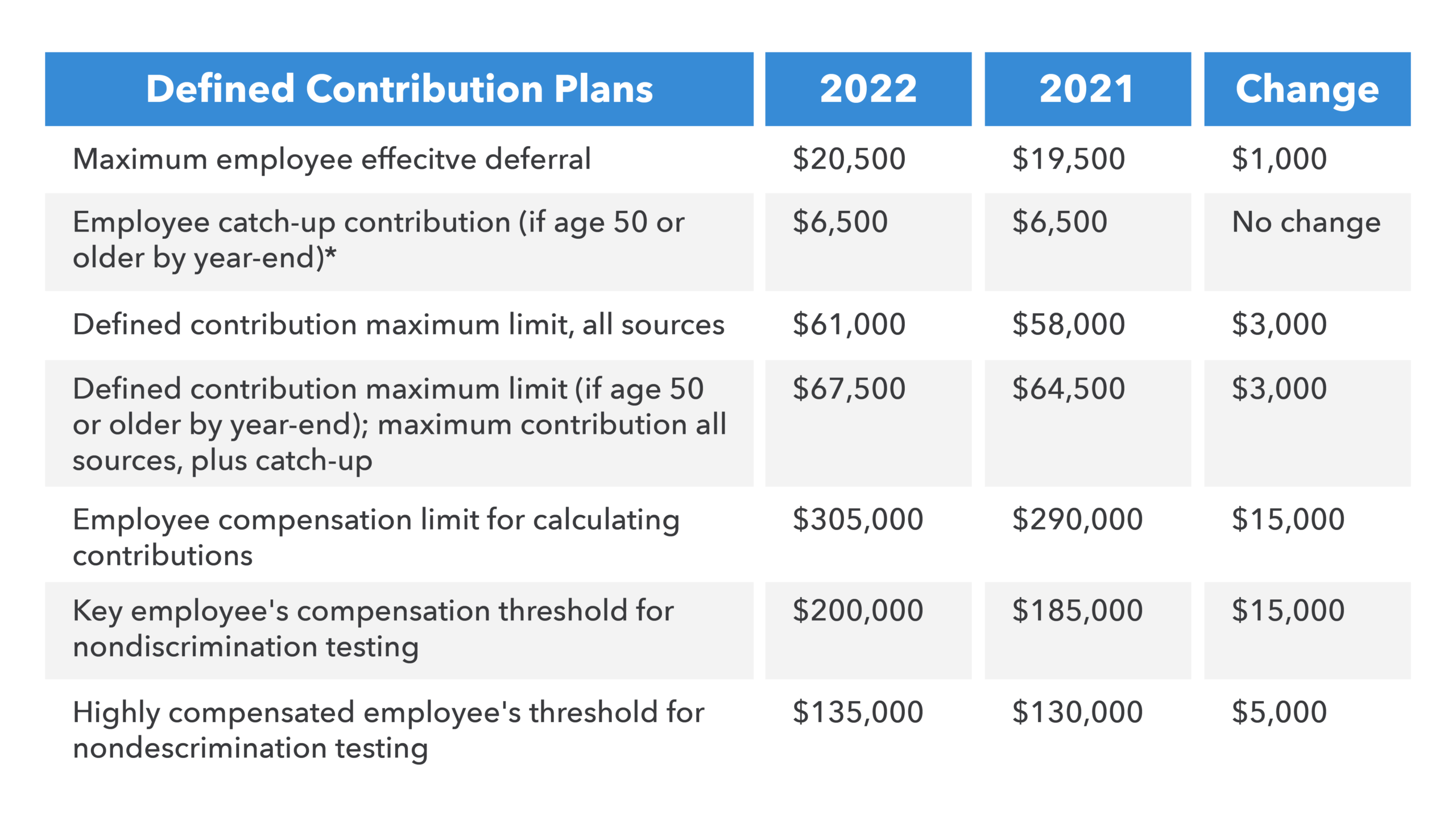

The 401(k) is one of the well-nigh woefully light retirement instruments ever invented. The maximum amount you can contribute is $twenty,500 for 2022, up from $19,500 in 2021. A 401k is part of your 3-legged retirement stool. The other two legs include your after-taxation investment accounts and your side hustles.

Although the 401(k) pales in comparing to a nicely funded pension, even more than disappointing than the 401k is the IRA. With the IRA retirement plan, you tin only contribute $6,000 in pre-tax dollars. Further, you tin can simply contribute if yous brand under $76,000 a year every bit an individual and $125,000 as a married couple. What about the rest of us?

Meanwhile, you take to make less than $140,000 a year as a unmarried person or $208,000 as a married couple for the privilege of contributing the maximum $half-dozen,000 in after- tax dollars to a Roth IRA. I do non recommend doing this earlier maxing out your 401(thousand).

Requite me a pension that pays lxx% of my last year'due south bacon for the residuum of my life over a 401k or IRA any time! At least with the 401(k), anybody can contribute.

Average 401(k) Retirement Balances

Based on Allegiance's 2020 study, here are the boilerplate retirement balances for the IRA, 401(k), and 403(b). Expect the balances to be 5-10% college for 2022.

- The boilerplate IRA balance was $111,500, a xiii% increase from last quarter. Information technology is slightly college than the boilerplate balance of $110,400 in 2019.

- The boilerplate 401(k) remainder increased to $104,400 in Q22020, a 14% increase from Q1 just downwardly two% from a yr ago. For 4Q2020, the boilerplate 401(thou) balance rose to roughly $120,000.

- Average 403(b) account residuum increased to $91,100. This is an increment of 17% from terminal quarter and upwardly 3% from a year ago.

Given the stock market has continued to do very well in 2021, the boilerplate 401k savings past historic period is likely up another 5% – 10% this yr.

The Average 401(grand) Residuum By Age

Let'south focus on the 401(k) and what people should have in their 401(yard) by age. The entire goal is to accumulate plenty money in your 401(yard) and other retirement accounts to somewhen live financially complimentary.

The average 401(thousand) residuum at the end of 2020 was roughly $120,000. Therefore, what should the 401(m) savings by age be today? Given the median historic period in America is about 36 years one-time, the boilerplate 36-year-old should have a 401(chiliad) balance of around $120,000. Unfortunately, $120,000 is even so pretty low.

Below is the average 40(1)k savings by age range as of 4Q2020 according to Fidelity. It's great to encounter the average 401k savings at retirement age rise to $229,100. However, that's still not enough to alive a comfortable retirement lifestyle.

As an educated reader who is logical and believes saving for retirement is a must, I've proposed a 401(1000) savings by age recommendation tabular array that shows how much each person should have s(a)ved in their 401k at age 25, 30, 35, twoscore, 45, l, 55, 60, and 65. The amounts are much greater than the average 401k savings past age in America.

We stop at 65 considering you are allowed to beginning withdrawing penalty complimentary from your 401(k) at age 59 1/2. Meanwhile, I pray to goodness you don't have to piece of work much past 65. By age 65, you will have had 40+ years to save and investment already!

401k Savings By Historic period: How Much Y'all Should Have

To determine how much you should have saved in your 401k by age, I've come with some assumptions that have encapsulated in a chart beneath.

The assumptions for the below chart are as follows:

- Depression End cavalcade accounts for lower maximum contribution amounts available to savers above 45.

- Mid Finish column accounts for lower maximum contribution amounts bachelor to savers below 45.

- High End cavalcade accounts for savers who are nether the age of 25. Later on the first yr, 1 maximizes their contribution every year to their 401k program without failure.

- Average starting working age is 22. But yous tin can follow the number of years working as a unlike guideline if you graduate later or before.

- $18,000 is used as the conservative base instance maximum contribution corporeality for one's entire working life.

- No afterwards-revenue enhancement income contribution, although more than power to you if you lot take the disposable income to do and so.

- The rate of return assumptions are between 0% – ten%.

- Company friction match assumption is between 0% – 100% of employee contribution. $61,000 is the total 401k contribution for 2022. Employees can contribute a maximum of $twenty,500.

- The Low, Mid, and High columns should successfully encapsulate about lxxx% of all 401K contributors who max out their contributions each yr. There volition be those with less, and those which much greater balances thanks to college returns.

- You are logical and not a knucklehead. Just by searching this topic, you lot are taking ownership of your retirement and are thinking ahead with an action plan.

Fiscal Samurai 401(one thousand) Savings Past Age Guide

Hither is my 401(k) savings targets by historic period.

From the results, nosotros can see that even after 38 years of consistent saving, yous'll but have around $one,000,000 to $five,000,000 in your 401k in a realistic cycle of bull and conduct markets. In other words, I believe everybody should become 401(chiliad) millionaires by 60.

If yous're just starting your 401(one thousand) savings journey, you could get lucky and attain the high finish column with consistent viii%+ annual growth and company profit sharing afterwards 38 years. Subsequently all, the maximum 401(one thousand) contributions volition be much higher over the next 38 years than the previous 38 years.

But it'southward most probable that most people reading this commodity should follow the eye-to-low end columns as a 401(k) savings guide. The median historic period in America is roughly 36. Meanwhile, the median age of a Financial Samurai reader is closer to 38.

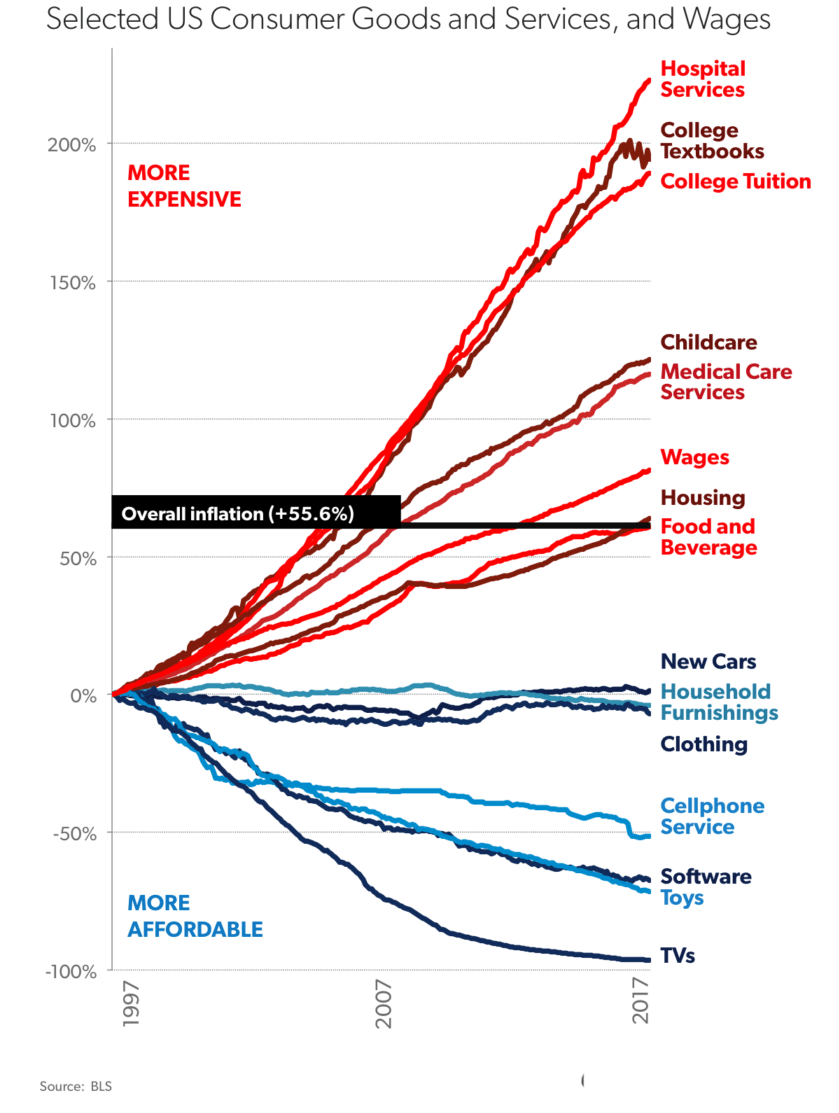

Investing Matters Because Inflation Matters

Let's say yous live for 25 years later retiring at 60. You only go to live on $40,000 – $100,000 a year on the depression-to-mid end. Sounds feasible in today'due south dollars, but not and then much in future dollars due to aggrandizement.

If goodness forbid you lot live for 35 years afterward retiring at threescore, so you can only live off of $28,571 – $71,000. If we use a ii% aggrandizement rate to calculate what $ane,000,000 – $v,000,000 is worth today, its only worth about $5500,000 – $two,355,000.

We know that due to inflation, a dollar today volition not go equally far as a dollar 30+ years from now. Private university tuition will probably price over $100,000 a year in 20 years. That is ridiculous since teaching is now free thanks to the internet.

Then in that location is the incredible growth of healthcare costs that is the about worrisome for retirees. For example, I've been paying $23,000+ a twelvemonth in healthcare premiums for a platinum plan for my family of iii. This is despite usa all in good health.

Does that sound affordable for the average American household who makes $68,000 a year? Absolutely not, which is why employees should non underestimate the value of their overall work benefits.

In fact, inflation is the reason why it takes $3 1000000 to be a real millionaire today. Make sure you own assets similar stocks, real estate, and more to let aggrandizement work for you!

To help grow your net worth, I recommend diligently tracking your net worth with Personal Capital. Applied science has come up a long way since tracking our money by hand or with an Excel spreadsheet. Remember, what is measured tin can be optimized.

Depend On Nobody Simply Yourself

Contribute the maximum pre-tax income you can to your 401(k) for as long as y'all work. This is the absolute MINIMUM y'all can practice to past on the right 401k savings by age path.

Below is a chart that shows what you could have in your 401(g) if you max it out each twelvemonth starting in 2022. The right paw cavalcade shows what y'all would take in your 401(k) with 8% compound almanac returns.

In other words, everybody who consistently maxes out their 401(k) each twelvemonth will likely be a 401(k) millionaire past the time they turn threescore.

After you contribute a maximum to your 401k every year, try and contribute at least twenty% of your later on-tax income after 401k contribution to your savings or retirement portfolio accounts.

This way, you will take potentially DOUBLE the corporeality in full retirement saving if your household income is $100,000 or more. If your household income is closer to $50,000, yous should still see a nice 30% boost to your retirement savings if you consistently salve twenty% of your subsequently revenue enhancement income. Hither is the recommended guild to contribute to your retirement accounts.

Care for your 401k just like Social Security and write it off completely from your mind. Practise not expect either accounts to be there for you when you retire. It's just like how you lot should never look the government to ever help you when you lot're in need.

Simply imagine 30 years from now, the authorities deciding to enhance penalty free 401k withdrawal to age 75 from 59.v? Unfortunately, yous need the coin at age 60. Because you withdraw, the government imposes a 30% penalty on pinnacle of the taxes y'all have to pay. Don't think information technology can't happen. Expect it to happen!

Taxable Investment Portfolio Is Key

The simply thing y'all can count on is later-tax money you've invested or saved. This is why subsequently maxing out your 401k, it'southward practiced to open an after-revenue enhancement brokerage account. Consistently contribute a percentage of your paycheck each mont into your taxable investment portfolio. I recommend at least xx%.

Your goal should exist to then build equally many passive income streams as possible. The more passive income streams and active income streams you have, the more financially gratis you will be.

Challenge yourself to raise your after-tax and 401k contribution savings percent to possibly 50%. It won't be easy. Just if yous practise raising your savings rate by 1% a calendar month until it hurts, you'll find it easier than y'all remember.

A straightforward fashion to maximum savings is to make your 401(chiliad) maximum contribution automated. Save every other paycheck for the rest of your working life.

Max out your 401k and save over l% of your later on-tax income for at to the lowest degree x years in a row. If you do, you will be financially gratuitous to practise whatever you desire!

Recommendation To Growing A Large 401(k)

Now that you know what the advisable 401k savings by historic period is, information technology'south time to manage your finances similar a hawk. To do so, sign upwardly for Personal Capital letter, the spider web's #1 gratuitous wealth management tool. Personal Capital will enable you to become a better handle on your finances.

In improver to better money oversight, run your investments through their award-winning Investment Checkup tool. I will bear witness you exactly how much y'all are paying in fees. I was paying $i,700 a twelvemonth in fees I had no idea I was paying.

After y'all link all your accounts, use their Retirement Planning calculator. Information technology pulls your real data to give you as pure an interpretation of your fiscal time to come as possible using Monte Carlo simulation algorithms. Definitely run your numbers to run across how y'all're doing.

To track my 401k savings past age guide yous must max out your 401k each year. With investments returns coupled with visitor matching, you'll be amazed how much you will accumulate over the years.

I've been using Personal Upper-case letter since 2012. In this fourth dimension, I have seen my net worth skyrocket thank you to better money management.

Build Wealth Through Real Manor

In addition to investing in stocks and bonds through your 401k, I recommend diversifying into real estate also. Existent estate is a core asset course that has proven to build long-term wealth for Americans. Information technology'due south of import to own a tangible asset that provides utility and a steady stream of income.

Given interest rates have come way down, the value of rental income has gone way upwards. The reason why is because it now takes a lot more capital to generate the same amount of hazard-adjusted income. Aggrandizement is picking upward steam, which further boosts the value of real estate.

With real estate, you can earn a steady stream of passive to semi-passive income well earlier age 59.5, which is when you can withdraw from a 401k penalty-gratis.

Two Favorite Existent Estate Platforms

Fundrise: A way for accredited and not-accredited investors to diversify into real estate through private eFunds and eREITs. Fundrise has been effectually since 2012 and has consistently generated steady returns, no matter what the stock market place is doing. For well-nigh investors, investing in a diversified portfolio is the best way to go.

CrowdStreet: A way for accredited investors to invest in individual existent estate opportunities more often than not in 18-hour cities. 18-60 minutes cities are secondary cities with lower valuations. They also have higher rental yields, and potentially higher growth due to job growth and demographic trends.

Both platforms are costless to sign upwards and explore.

I've personally invested $810,000 in existent manor crowdfunding across 18 projects. My goal is to accept advantage of lower valuations in the heartland of America. My existent manor investments business relationship for roughly 50% of my current passive income of ~$300,000.

Follow my 401k savings by historic period guide. But in the meantime, as well build a passive income portfolio and then you tin can alive a meliorate life today. Given you cannot withdraw from your 401k without penalty until 59.5, it is your passive investment portfolio that matters even more than.

Buy The Best Selling Personal Finance Book

If y'all want to drastically improve your chances of achieving financial liberty, purchase a hard re-create of my new volume, Buy This, Not That: How To Spend Your Way To Wealth And Freedom. The volume is jam packed with unique strategies to assistance you build your fortune while living your all-time life.

Buy This, Not That is already a #1 new release and #one all-time seller on Amazon. By the time you finish BTNT you will gain at to the lowest degree 100X more value than its cost. After spending xxx years working in finance, writing virtually finance, and studying finance, I'm certain y'all will beloved Buy This, Not That. Thank you for your back up!

How Much Should I Have Saved In My 401k Past Age is a Financial Samurai original post. Everything is written based off starting time hand feel because money is too important to be left upward to pontification.

Source: https://www.financialsamurai.com/how-much-should-one-have-in-their-401k-at-different-ages/

Posted by: kohndeabinder.blogspot.com

0 Response to "At What Age Do You Have To Draw From Your 401k"

Post a Comment